EMPOWERMENT

YOUR BUSINESS

YOUR WAY

BUT... BETTER

With the power of NANO, our proprietary LOS, we help Loan Officers dominate their market with better pricing, tech, and processes.

Recieve a Margin Analysis

Proforma Review

Process review

Processing Timeline

Introduction to Nano

Our Vision is

simple,

We're building a better mortgage experience. We've made it our mission to build the best mortgage experience through innovative technology, competitive pricing, and building stronger relationships.

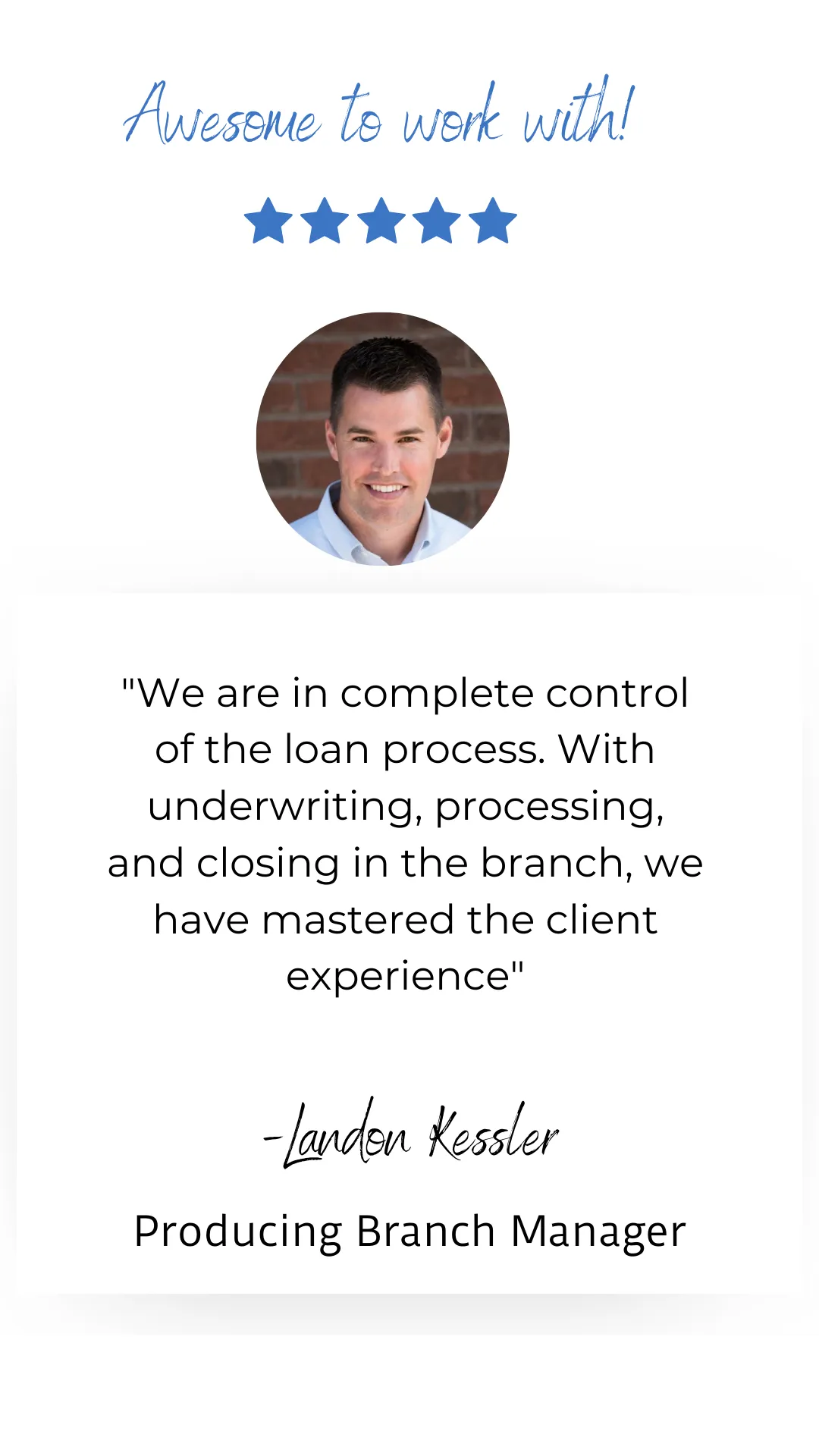

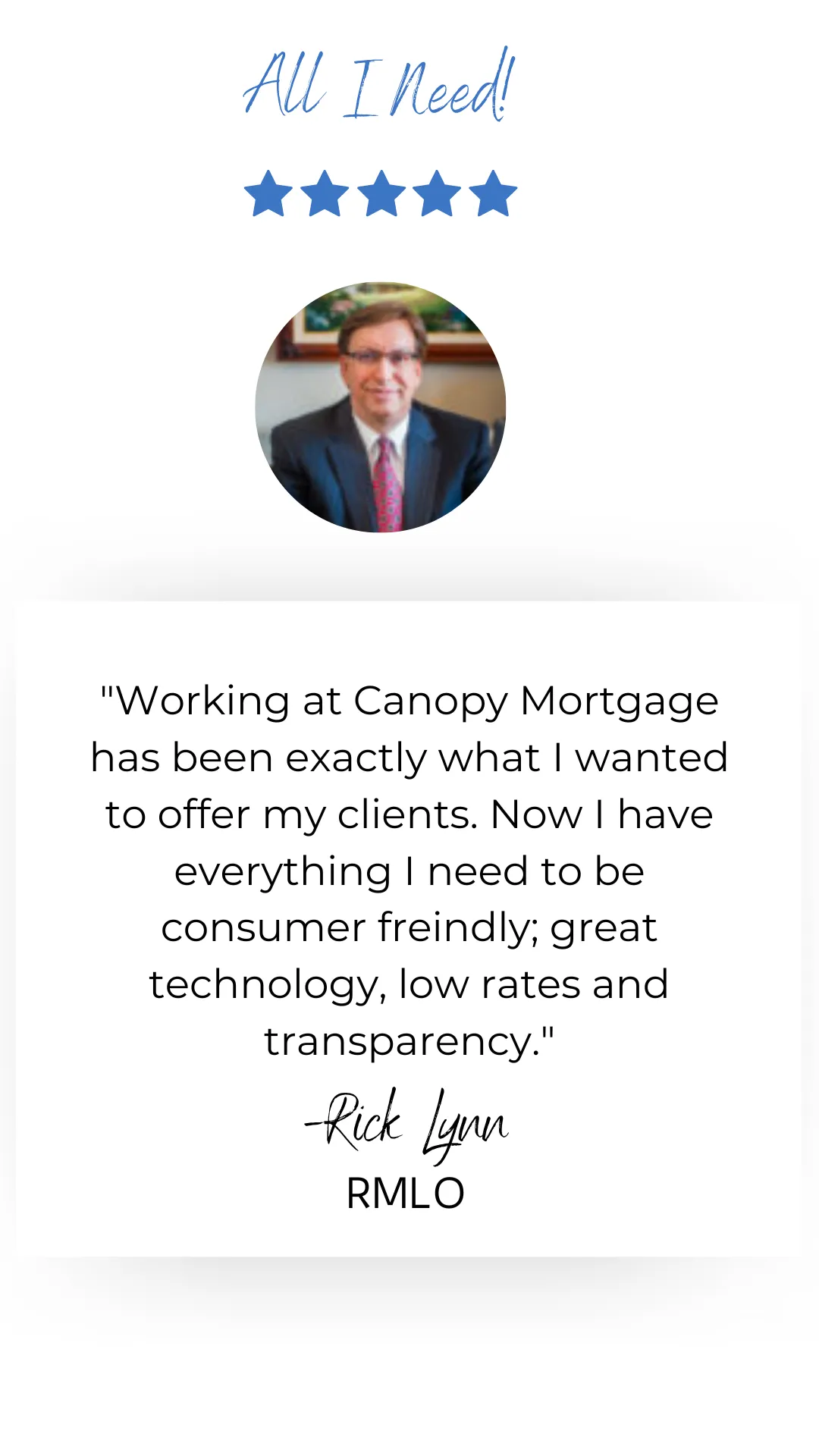

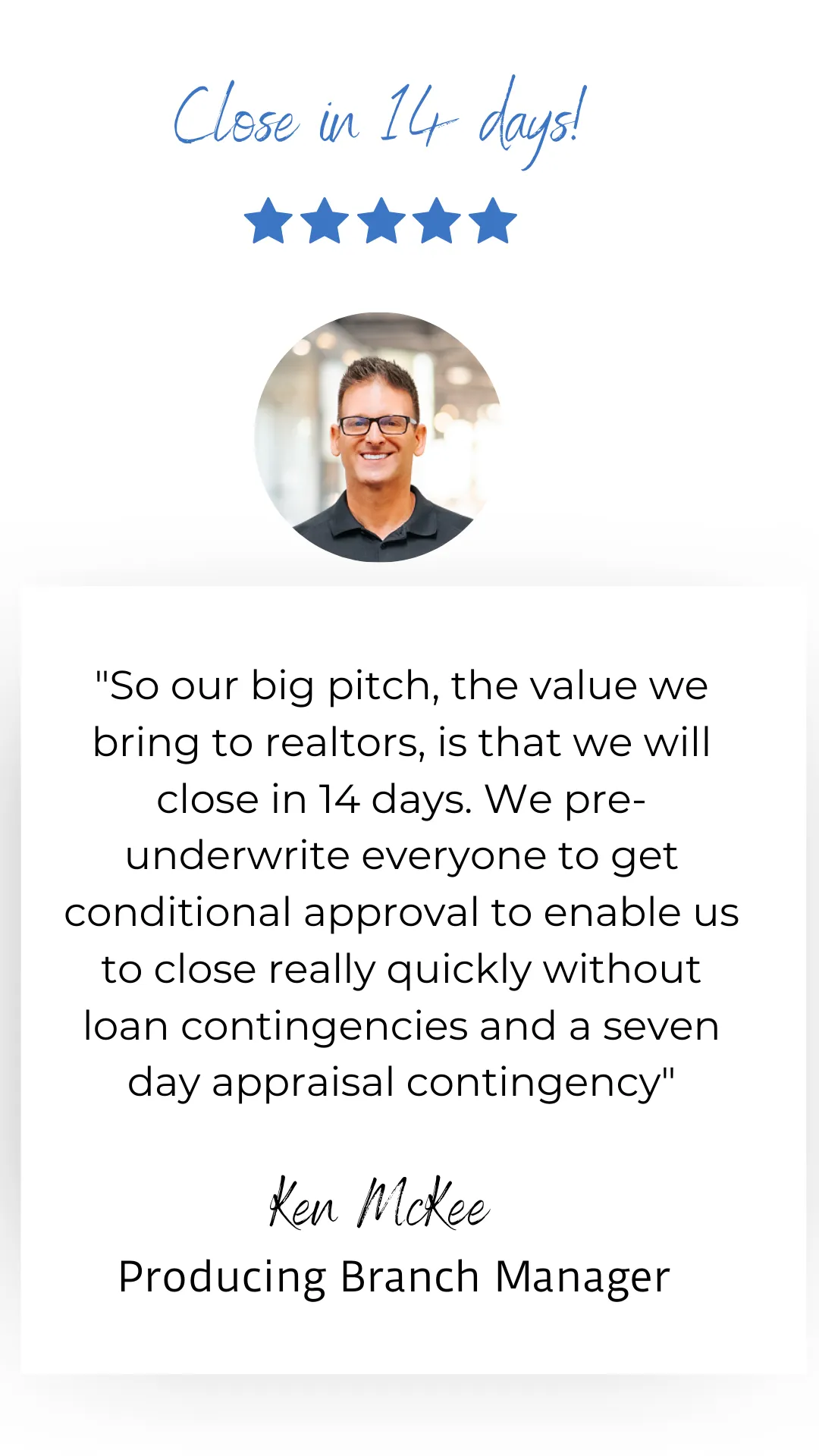

Testimonials

MORTGAGE WITH CONFIDENCE

Secure Approvals

In-House Processing, Underwriting & Closing

Save Time & Money

Great Rates, Low Fees,

& Simple Process

Peace of Mind

Close-on-Time

as fast as 7 days

THINGS WE'VE DONE FOR OUR CLIENTS

Construction Loans

We offer conventional and FHA one-time closes.

2/1 Temporary Buydown

A 2-1 buydown is a type of financing that effectively lowers the interest rate on a mortgage for the first two years before it rises to the regular, permanent rate. The rate is typically two percentage points lower during the first year and one percentage point lower in the second year. A seller concession pays for the effective interest rate reduction.

Renovation Loans

ChoiceRenovation for conventional and 203K (Full & Standard) options to offer borrowers

Applied MCC Tax Credits

Mortgage Credit Certificates (“MCCs”) is a dollar-for-dollar tax credit for qualified recipients to increase housing payment affordability. In some cases, MCCs can also help borrowers who might not otherwise qualify for a loan by increasng thier qualifying income. See IRS form 8396

Down Payment Assistance

Down Payment Assistance is the financial support provided to homebuyers, from Texas Housing Non-Profits, to help cover the initial payment required when purchasing a home. It can come in the form of grants or loans and is typically aimed at assisting individuals or families who may have difficulty affording the down payment on their own.

Reverse Mortgages

Seniors aged 62 or older, can convert a portion of their home's equity into cash (to payoff bills, bolster retirement assets or savings). The remaining portion of equity is utilized to pay the interest of the loan for as long as the senior resides in the home. This allows the senior to access the value of their home without selling it or making monthly mortgage payments, which can help to alleviate the financial burden of a reduced income in retirement.

Closed Loans in 7 days

According to Ellie Mae, the average conventional loan took 57 days to process, FHA and VA loans took longer with an estimated 63 days. canopy mortgages proprietary Loan Origination Software, Nano and Our TLC team have cut the process to days, with an average application to Clear-To-Cose approval of 17 days and yes, we've closed loans in as little as seven days.

Streamline Refinances

Experience Effortless Closings: From FHA Streamlines to VA IRRLs, we've successfully closed numerous streamline loans with minimal documentation, simplified credit reviews, and appraisal waivers.

Approved Loans Banks Denied

Turning Denials into Approvals: Through innovative loan products and effective solutions, we've successfully secured loans that were previously denied by other lenders and banks.

E-Closings

Experience the Future of Mortgage Closings: E-Closing is the modern way to finalize your mortgage, conducted securely in a digital environment where many or all closing documents are signed electronically. It's a convenient solution, especially for buyers unable to attend in-person signings with the title company

Bank Statement Loans

A bank statement mortgage, also known as a bank statement loan, is a type of mortgage that allows individuals, often self-employed or those with non-traditional income sources, to qualify for a home loan using their bank statements instead of traditional income documentation like tax returns or pay stubs

DSCR Loans

A DSCR mortgage, or Debt Service Coverage Ratio mortgage, is a type of loan used by real estate investors. It usest he rental income generated by an investment property to qualify rather than relying on personal income when determining eligibility for a mortgage

E. Lee Smith

Growth Leader NMLS#436498

512-948-6550

Esmith@canopymortgage.com

Contact Me Today For a Discreet Conversation About Canopy Mortgage

E. Lee Smith

Branch Manager

RMLO

NMLS: 436498

512-948-6550

Branch: Canopy Mortgage - TLC Group - 13809 Research Blvd, Ste 500, Austin, TX 78750 | Office #512-598-9093 | NMLSConsumerAccess.org #: 1359687 | Equal Housing Lender -All loans subject to credit and property approval.

Consumers wishing to file a complaint against a banker or a residential mortgage loan originator should complete and send a complaint form to the Texas department of savings and mortgage lending, 2601 North Lamar, suite 201, Austin, Texas 78705. Complaint forms and instructions may be obtained from the department’s website at www.sml.texas.gov. A toll-free consumer hotline is available at 1-877-276-5550. The department maintains a recovery fund to make payments of certain actual out of pocket damages sustained by borrowers caused by acts of licensed residential mortgage loan originators. A written application for reimbursement from the recovery fund must be filed with and investigated by the department prior to the payment of a claim. For more information about the recovery fund, please consult the department’s website at www.sml.texas.gov. State Licenses page, Privacy Policy, and Terms of Use

Instagram

LinkedIn

Youtube